Why Your Age and Life Stage Matter When Choosing Mutual Funds

Here’s something most investors discover eventually: the investment approach that worked brilliantly in your twenties often feels completely wrong in your fifties. And that’s not just normal – it’s financially smart.

Think about it: A 25-year-old software engineer with her first salary can handle market volatility very differently than a 58-year-old manager planning retirement in two years. They have fundamentally different timelines, different financial responsibilities, and different capacities to weather market storms.

The young professional has three decades to recover from a market crash. The near-retiree has maybe two years, and needs that money to start generating income soon. Same investment product, completely different appropriateness.

This guide explains how mutual fund risk levels generally align with different life stages, from your first job through retirement and beyond. But here’s what’s critical to understand upfront: this is an educational framework, not personal advice.

Your actual investment choices should come from:

- Honest self-assessment: Evaluate your own risk tolerance, time horizon, financial goals, and current obligations realistically – not optimistically

- Professional guidance: Consult an AMFI-registered mutual fund distributor or SEBI-registered investment advisor who can assess your specific situation comprehensively

- Due diligence: Carefully review all fund documents (Scheme Information Document, Key Information Memorandum, etc.) before investing a single rupee

Let’s explore how this works across different life stages.

Important Notice: This article is purely educational and does not constitute investment advice, recommendation, or solicitation to invest. Mutual fund investments carry market risks, always read all scheme documents carefully before investing. Investment decisions should align with your personal financial situation, risk tolerance, and goals. Past performance doesn’t guarantee future results.

Understanding Risk in Mutual Funds: What Does It Actually Mean?

When financial professionals talk about “risk” in mutual funds, they’re primarily discussing volatility, how much your investment value can swing up and down due to market movements.

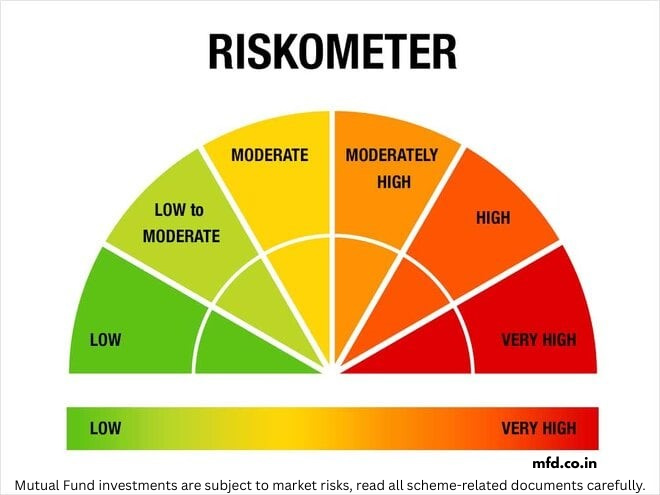

The SEBI Risk-o-meter: Your Starting Point

SEBI requires every mutual fund scheme to display a “Risk-o-meter” with six levels:

- Low

- Low to Moderate

- Moderate

- Moderately High

- High

- Very High

Think of this as a volatility gauge or earthquake scale for investments:

- A “High” risk scheme might drop 25-35% during a market crash but could also deliver 15-18% returns over a 10-year period

- A “Low” risk scheme might barely budge during crashes, maybe dropping just 2-5% – but will also deliver more modest returns, perhaps 5-7% annually

The Critical Distinction Most Investors Miss

Here’s what catches many investors off-guard: The Risk-o-meter shows the fund’s inherent volatility characteristics – NOT whether that fund is right for you.

A “Very High” risk small-cap fund might be perfectly appropriate for a 27-year-old investing for retirement in 35 years. That same fund could be completely inappropriate – even dangerous – for a 62-year-old needing income in 18 months.

Suitability depends entirely on your personal circumstances: time horizon, financial obligations, emotional temperament, existing corpus, and income stability.

Why Your Appropriate Risk Level Changes as You Age

Your suitable risk level isn’t fixed at birth – it evolves continuously based on several interconnected factors:

1. Time Horizon: The Master Variable

How many years until you actually need this money?

- A 25-year-old investing for retirement at 60 has a 35-year horizon – enough time to ride out multiple market cycles, crashes, and recoveries

- A 62-year-old planning to retire at 65 has a 3-year horizon – barely enough time to recover from one significant market decline

Time is your most powerful risk management tool. The longer your horizon, the more short-term volatility you can theoretically withstand because you have years for markets to potentially recover.

2. Income Stability and Continuity

Can you keep investing consistently even when markets drop 30-40%?

Someone with a stable government job or tenured corporate position can generally maintain SIP contributions through market downturns. A freelance consultant with variable income might need to pause investments during lean months – potentially selling at the worst possible times to cover expenses.

Your income stability directly affects your practical risk capacity.

3. Emergency Cushion: The Non-Negotiable Foundation

Do you have 6-12 months of living expenses in completely safe, immediately accessible accounts?

This separate emergency fund sitting in savings accounts, liquid funds, or fixed deposits is absolutely crucial. It prevents you from being forced to sell equity investments during market crashes to cover unexpected expenses.

Example: Rahul keeps ₹3.5 lakh in a savings account (covering 6 months of his ₹58,000 monthly expenses). This cushion means that when his laptop died unexpectedly during the March 2020 market crash (when his equity SIP was down 35%), he could buy a new one from his emergency fund without touching his battered investments – which recovered fully within 18 months.

Emergency fund first. Aggressive investments second. Always.

4. Financial Obligations and Responsibilities

What are your current financial commitments?

Compare these two 40-year-olds:

Priya: Single, no dependents, renting, no loans, stable job. Monthly expenses ₹40,000.

Arjun: Married, two children, ₹35,000 home loan EMI, ₹15,000 school fees, supporting aging parents. Monthly obligations ₹85,000.

Even if both earn ₹1.5 lakh monthly, Arjun has dramatically lower risk capacity. A job loss or market crash affects him much more severely. His appropriate risk level is inherently lower because his financial obligations leave less margin for error.

5. Accumulated Wealth: Absolute vs. Percentage Losses

Someone with ₹5 lakh invested thinks very differently than someone with ₹2 crore.

Consider a 20% market decline:

- ₹5 lakh becomes ₹4 lakh (₹1 lakh loss – painful but recoverable)

- ₹2 crore becomes ₹1.6 crore (₹40 lakh loss – psychologically devastating, potentially retirement-altering)

As your corpus grows, the absolute rupee value of percentage declines becomes harder to stomach psychologically, even if your theoretical time horizon hasn’t changed. A 25% drop might feel academic when you have ₹3 lakh invested. That same 25% drop on ₹1.5 crore feels catastrophic.

6. Emotional Tolerance: Theory vs. Reality

Can you actually sleep at night when your portfolio drops 25%?

Many investors dramatically overestimate their risk tolerance until markets actually fall. They answer risk questionnaires optimistically: “Yes, I can handle 30% volatility for long-term gains!”

Then markets drop 25% in six weeks, and they panic-sell at the bottom, crystallizing losses and destroying their long-term strategy.

There’s absolutely no shame in knowing your psychological limits. A conservative investor who stays the course earns better returns than an aggressive investor who panic-sells during every correction.

The General Principle (With Major Caveats)

Longer time horizons + greater capacity to handle volatility = potential to consider higher-risk investments

But this is deeply personal and depends on your complete financial picture – income, obligations, corpus size, goals, temperament, and life circumstances. Cookie-cutter rules don’t work.

Young Professionals (Age 22-35): The Long Runway Advantage

Your Typical Life Stage Characteristics

If you’re in this phase, you typically have:

- Long investment horizon: 25 to 35+ years until retirement – potentially your entire working career ahead

- Rising income trajectory: Regular salary increments, skill development, career growth

- Relatively few financial dependents: Perhaps no children yet, parents still working

- Time to recover from downturns: Multiple decades to ride out crashes and capture multiple market cycles

- Generally higher volatility capacity: Ability to tolerate portfolio swings without immediate financial impact

Thinking About Risk at This Stage

With decades stretching ahead, this life stage often supports considering equity-oriented mutual funds – those with SEBI Risk-o-meter ratings of “Moderate” to “High” or even “Very High.”

Why equity orientation makes sense here:

You have time – your most valuable asset. If markets crash 40% when you’re 28, you potentially have 30+ years for recovery and subsequent growth. Historical market data (though not predictive of future results) suggests that equity investments, despite severe short-term volatility, have tended to deliver stronger returns over extended multi-decade periods.

Real-world perspective: Investors who started SIPs in 2008 right before the global financial crisis (when markets fell roughly 60% over 12 months) and continued investing through the crash experienced substantial recovery and growth over the subsequent 10-15 years – but only if they didn’t panic and sell at the bottom.

Time exposure helps you capture multiple market cycles – the crashes and the subsequent recoveries and bull runs.

Illustrative Fund Categories Young Professionals Sometimes Explore

(These are purely educational examples, not recommendations. Always consult an AMFI-registered distributor or SEBI-registered advisor before investing.)

Flexi-cap, Multi-cap, or Large & Mid-Cap Funds:

- Diversified equity exposure across different company sizes

- Balances growth potential with some stability from large-cap holdings

- Typical Risk-o-meter: Moderately High to High

Mid-Cap and Small-Cap Funds:

- Higher volatility potential with corresponding higher return possibilities

- Typically used as a smaller portion (15-25%) of overall portfolio

- Typical Risk-o-meter: High to Very High

ELSS (Equity-Linked Saving Scheme):

- Combines Section 80C tax-saving benefits (up to ₹1.5 lakh deduction) with equity exposure

- 3-year lock-in period – shortest among all 80C options

- Typical Risk-o-meter: Moderately High to High

Aggressive Hybrid Funds:

- Majority equity (typically 65-80%) with some debt (20-35%) for slight stability

- Slightly lower volatility than pure equity funds

- Typical Risk-o-meter: Moderately High

The Mathematical Power of Time: A Compelling Example

Consider two investors, both investing ₹10,000 monthly:

Investor A (Age 25): Invests for 35 years until retirement at 60

- Assuming 12% annualized return: Final corpus approximately ₹6.44 crore

- Total invested: ₹42 lakh

- Gains: ₹6.02 crore (1,333% return)

Investor B (Age 40): Invests for 20 years until retirement at 60

- Same 12% return: Final corpus approximately ₹99.91 lakh

- Total invested: ₹24 lakh

- Gains: ₹75.91 lakh (316% return)

Starting 15 years earlier doesn’t just add gains – it multiplies them exponentially through compounding. This is why even modest amounts invested young can become substantial wealth.

(Note: These calculations are illustrative only, assuming constant returns which never occur in reality. Actual market returns vary dramatically year-to-year, and past performance doesn’t guarantee future results.)

Critical Non-Negotiable: Emergency Fund First

Even with high risk tolerance and a 35-year horizon, you absolutely must have 6-12 months of living expenses in completely liquid, safe accounts before investing aggressively in equity funds.

Why this matters: Life happens without consulting your investment timeline.

- Job losses during economic downturns

- Medical emergencies requiring immediate cash

- Home repairs that can’t wait

- Family obligations that appear suddenly

If you’re forced to sell equity investments during a 30% market crash to cover emergency expenses, you:

- Crystallize losses by selling at depressed prices

- Miss the subsequent recovery when markets rebound

- Destroy your long-term compounding strategy

- Create enormous psychological stress during already difficult times

The right sequence: Build emergency fund → max out ELSS for tax saving → invest in equity funds for long-term goals

Never reverse this order.

Behavioral Trap to Avoid: Overconfidence in Volatility Tolerance

Many young investors have never experienced a real bear market. They started investing in 2020 after the crash, riding the subsequent bull run, and assume they can handle 30-40% declines easily.

Then markets actually fall 35% over three months, their ₹5 lakh portfolio drops to ₹3.25 lakh, financial media screams about recession, colleagues panic-sell, and suddenly their theoretical risk tolerance evaporates.

Reality check: If you haven’t lived through watching your portfolio decline significantly, you don’t truly know your emotional risk tolerance yet. Start conservatively, increase equity exposure gradually as you gain experience and confidence.

Mid-Career Professionals (Age 35-50): Balancing Growth with Protection

Your Typical Life Stage Characteristics

If you’re in this phase, you’re likely experiencing:

- Moderate time horizon: 10 to 25 years until retirement – still significant, but notably shorter than before

- Peak earning years: Highest salary of your career, maximum income potential

- Peak financial responsibilities: Home loan EMIs (₹25,000-50,000), children’s school/tuition fees (₹15,000-30,000), potentially supporting aging parents

- Substantial accumulated corpus: Perhaps ₹15 lakh to ₹1 crore already invested – the most wealth you’ve ever managed

- Moderate volatility capacity: Can tolerate some declines, but cannot afford catastrophic losses that derail major upcoming goals

- Growing awareness of retirement: No longer an abstract concept – starting to calculate actual numbers needed

The Fundamental Shift in Thinking

This is where investment strategy becomes genuinely complex. You face competing pressures:

Growth imperative: You still need substantial corpus growth to reach retirement and education funding goals. Inflation-beating returns remain essential.

Protection imperative: You’ve accumulated significant wealth that took 10-15 years to build. A 50% market crash could set you back a decade – time you no longer have.

Obligation constraints: Your monthly financial commitments are at their highest. You have less flexibility to pause investments or delay withdrawals during market downturns.

Rethinking Risk at This Stage

Investors in this stage with moderate risk capacity often explore balanced approaches – mixing equity-oriented schemes (for continued growth potential) with debt-oriented schemes (for downside protection and stability).

Common Risk-o-meter range: “Moderate” to “Moderately High” – stepping down from the “High” to “Very High” range appropriate for younger investors.

Illustrative Fund Categories Mid-Career Professionals Sometimes Explore

(Purely educational examples – not recommendations)

Large-Cap and Flexi-Cap Funds:

- Equity exposure focused on established, stable companies

- Less volatility than mid/small-cap funds

- Still provides equity returns potential

- Risk-o-meter: Moderate to Moderately High

Balanced Advantage or Dynamic Asset Allocation Funds:

- Automatically adjust equity-debt mix based on market valuations

- Increase debt during market peaks, increase equity during crashes

- Removes emotion and timing decisions from rebalancing

- Particularly valuable when you’re too busy with career/family to actively monitor markets

- Risk-o-meter: Moderate to Moderately High

Aggressive or Conservative Hybrid Funds:

- Pre-mixed portfolios combining equity and debt in relatively fixed proportions

- Aggressive hybrid: 65-80% equity, 20-35% debt

- Conservative hybrid: 25-35% equity, 65-75% debt

- Choose based on your specific risk capacity and goal timelines

- Risk-o-meter: Moderate (conservative) to Moderately High (aggressive)

Multi-Cap or Large & Mid-Cap Funds:

- Diversified equity exposure with limited allocation to more volatile mid-caps

- Balances growth potential with relative stability

- Risk-o-meter: Moderately High

Small/Mid-Cap Funds:

- Only in small portions (10-20% of portfolio maximum), if your risk capacity genuinely allows

- Provides growth potential but adds significant volatility

- Risk-o-meter: High to Very High

Why Portfolio Balance Becomes Critical

Here’s the reality check for 45-year-olds:

If markets crash 50% (as happened in 2008), you don’t have 30 years to recover – you have perhaps 15-20 years. During those 15-20 years, you’ll face major, inflexible financial obligations:

- College tuition bills arriving exactly on schedule regardless of market conditions

- Home loan principal prepayment targets to reduce retirement debt burden

- Children’s wedding expenses within specific timeframes

- Potential parental care costs that can’t be delayed

A 100% equity portfolio crashing from ₹50 lakh to ₹25 lakh right when your daughter’s engineering admission fee is due creates a catastrophic forced-selling scenario.

A balanced portfolio – say 60% equity (₹30 lakh) and 40% debt (₹20 lakh) – might decline to ₹35 lakh total (₹15 lakh equity, ₹20 lakh debt). The debt portion remains stable, providing liquidity for immediate needs without forcing equity sales at depressed prices.

The Time-Based De-Risking Principle

As specific major goals approach, consider gradually reducing equity exposure for that goal’s specific corpus:

Example: Children’s Higher Education Fund

- 10 years before goal (child is 8): 80% equity, 20% debt

- 7 years before (child is 11): 70% equity, 30% debt

- 5 years before (child is 13): 50% equity, 50% debt

- 3 years before (child is 15): 30% equity, 70% debt

- 1 year before (child is 17): 10% equity, 90% debt

- Goal year (admission): 0% equity, 100% short-duration debt/liquid funds

This glide path creates smooth de-risking without sudden exposure changes. You’re systematically moving money from volatile to stable instruments as the goal approaches, protecting accumulated wealth from last-minute market crashes.

Critical point: This applies to specific goal-based corpus, not your entire portfolio. Your retirement corpus (still 15+ years away) can remain more aggressively invested even while you’re de-risking the education fund.

Common Mistake: The “One More Year” Trap

Many mid-career investors maintain aggressive 80-90% equity portfolios thinking “I’m 45, still young, retirement is far away.” Then suddenly they’re 55, equity markets are booming, and they’re reluctant to de-risk because “markets are doing so well – I’ll do it next year.”

Then a market crash hits at age 57-58, wiping out 30-40% of their retirement corpus with just 2-3 years to recover. This sequence-of-returns nightmare is devastatingly common.

Solution: Start gradual de-risking in your mid-40s. Don’t wait until your late 50s. The glide path should begin early and proceed steadily.

Pre-Retirees (Age 50-60): Protecting What You’ve Built

Your Life Stage Characteristics

This critical decade brings fundamental changes:

- Short time horizon: Just 5 to 15 years until retirement – barely one or two market cycles

- Substantial accumulated corpus: Possibly ₹50 lakh to ₹3 crore – the most wealth you’ve ever managed in your life

- Limited recovery time: No longer have decades to bounce back from severe market losses

- Approaching income cessation: Salary stops at retirement; investments must generate replacement income

- Lower loss capacity: Major portfolio declines directly threaten retirement security and lifestyle

- Increasing healthcare costs: Age-related medical expenses rising, insurance premiums increasing

- Crystallizing retirement numbers: No longer abstract – you can calculate exactly how much you need

The Paradigm Shift: Capital Preservation vs. Growth

At this stage, the investment philosophy fundamentally shifts:

Ages 25-40: Growth at (reasonable) risk → “How can I build wealth fastest?”

Ages 40-50: Balanced growth and protection → “How do I keep growing while protecting what I have?”

Ages 50-60: Protection with measured growth → “How do I safeguard this corpus while still beating inflation?”

You’ve spent 25-30 years accumulating wealth. The primary objective now is don’t lose it while maintaining enough growth to combat inflation over a 25-30 year retirement.

Thinking About Risk in Pre-Retirement

Investors in this stage with lower risk capacity often focus primarily on debt and conservative schemes, with smaller, strategic equity exposure.

Common Risk-o-meter range: “Low” to “Moderate” – a significant step down from earlier career stages.

Illustrative Fund Categories Pre-Retirees Sometimes Explore

(Educational examples only)

Conservative Hybrid Funds:

- Primarily debt-oriented (65-75%) with small equity component (25-35%)

- Equity portion provides some inflation protection and modest growth

- Debt portion provides stability and capital preservation

- Risk-o-meter: Low to Moderate

Balanced Advantage Funds:

- Dynamic allocation positioned more conservatively as you approach retirement

- Typically tilts toward higher debt allocation during high market valuations

- Provides automatic risk management

- Risk-o-meter: Moderate

Debt-Oriented Hybrid Funds:

- Majority debt (85-90%) with minimal equity (10-15%)

- Very conservative, focused on stability

- Risk-o-meter: Low to Moderate

Short-Duration or Corporate Bond Funds:

- Pure debt exposure with minimal interest rate risk

- Focus on capital preservation and stable income

- Suitable for corpus needed within 2-5 years

- Risk-o-meter: Low to Low-Moderate

Limited Equity Exposure (if included):

- Typically capped at 20-35% of total portfolio maximum

- Invested exclusively in large-cap funds for relative stability and liquidity

- Gradually reduced as retirement approaches

- Serves only to combat inflation, not primary growth engine

Understanding Sequence of Returns Risk: A Critical Concept

This is arguably the most important risk concept for pre-retirees, yet it’s often overlooked.

The Problem: When you experience returns matters enormously – not just the average return over time.

Example: Two Investors, Same Average Return, Vastly Different Outcomes

Both Ramesh and Suresh retire at 60 with ₹1 crore, withdrawing ₹5 lakh annually (5% withdrawal rate). Both experience an average 7% annual return over 20 years – but in different sequences.

Ramesh: Experiences strong 15% returns in years 1-5, then moderate 3-5% returns in years 6-20

- Portfolio grows initially despite withdrawals

- Later withdrawals come from a larger base

- Corpus lasts 25+ years

Suresh: Experiences terrible -10% to 0% returns in years 1-5, then strong 10-15% returns in years 6-20

- Portfolio crashes early while still making withdrawals

- Forced to sell more units at depressed prices to maintain ₹5 lakh withdrawals

- Even with strong later returns, corpus depletes by year 18-20

Same average return. Dramatically different outcomes.

The sequence – particularly returns in the first 5-10 years of retirement – determines success or failure. This is why capital preservation becomes absolutely critical in your 50s.

The Inflation Dilemma: Why 100% Debt Is Also Risky

Here’s the counter-intuitive challenge: going entirely into debt funds too early creates its own significant risk – inflation erosion over 25-30 year retirement.

Consider:

- You retire at 60 with ₹1 crore in pure debt funds earning 6-7% annually

- Inflation averages 6% annually over your retirement

- Your real return (after inflation) is 0-1%

- By age 85, your purchasing power has been devastated despite no nominal loss

Real-world example: ₹50,000 annual expenses at age 60 require approximately ₹1.65 lakh at age 85 (assuming 5% inflation). Pure debt returns barely keep pace.

The Balanced Solution: Strategic Equity Allocation in Pre-Retirement

Many financial planning professionals suggest maintaining some equity exposure (typically 20-35% depending on individual risk capacity) even in the pre-retirement decade, invested exclusively in stable large-cap funds.

Rationale:

- Equity portion combats inflation over long retirement (25-30 years)

- Large-cap equity historically less volatile than mid/small-caps

- Debt portion (65-80%) provides stability and withdrawal reserves

- Balance protects against both market crashes AND inflation erosion

Critical caveat: Appropriate equity allocation is deeply individual. Someone with ₹3 crore corpus and modest expenses might maintain 35% equity comfortably. Someone with ₹40 lakh corpus and high expenses might need to stay at 15-20% equity maximum.

For specific guidance on appropriate allocation for your situation, consult an AMFI-registered distributor or SEBI-registered investment advisor.

Practical Action Steps for Pre-Retirees

1. Calculate Exact Retirement Number:

- Current monthly expenses: ₹______

- Adjusted for inflation to retirement: ₹______

- Multiply by 300-400 for required corpus (depends on withdrawal rate assumptions)

- Gap between current corpus and required corpus = continued savings needed

2. Separate Goal Buckets:

- Retirement corpus (managed separately with appropriate de-risking glide path)

- Children’s wedding fund (specific timeline, specific de-risking schedule)

- Emergency medical reserve (highly liquid, completely safe)

- Discretionary goals (travel, hobby, etc.)

3. Begin Gradual De-Risking:

- Don’t wait until 59 to suddenly shift from 80% equity to 30%

- Start systematic de-risking from age 50 or even earlier

- Annual rebalancing toward lower equity exposure

- Document your glide path and stick to it without emotional deviation

4. Stress Test Your Plan:

- What happens if markets crash 40% in year 58-59?

- Can you delay retirement by 2-3 years if needed?

- Do you have backup income sources (rental income, consulting)?

- Is your spouse’s income factored in?

5. Eliminate Debt Before Retirement:

- Clear home loans completely before age 60 if possible

- No outstanding personal loans or credit card debt

- Enter retirement with zero EMI obligations

- This dramatically reduces required monthly income

Retirees (Age 60+): Stability, Income Generation, and Longevity Planning

Your Life Stage Characteristics

Retirement has arrived or is imminent:

- Investment corpus now funds daily life: No longer hypothetical wealth – it pays for groceries, utilities, healthcare

- Systematic withdrawals for cash flow: Regular monthly/quarterly income from investments replaces salary

- Very low loss capacity: Cannot afford significant portfolio declines without lifestyle impact

- No new employment income: No recovery mechanism for losses through additional earnings

- Potentially long time horizon: With increasing life expectancy, 20-30+ years of retirement is common – longer than many careers

- Rising healthcare costs: Medical expenses typically increase with age, insurance becomes more expensive or unavailable

- Fixed Social Security: Whatever pension/EPF you have is mostly fixed, doesn’t increase with inflation

The Retirement Paradox: Conservative Yet Long-Term

Here’s the challenge that confuses many retirees:

You need maximum stability because you cannot afford losses – but you also need inflation protection because retirement might last 25-30 years.

100% ultra-conservative allocation solves the first problem but creates the second. 100% equity allocation solves the second problem but creates catastrophic versions of the first.

The solution lies in thoughtful balance and reserves management.

Risk Approach in Retirement

This stage typically requires very low-volatility schemes for the majority of portfolio, focused on capital stability and predictable income generation.

Common Risk-o-meter range: “Low” for 70-80% of portfolio, with possible “Low to Moderate” for a small long-term inflation-protection component.

Illustrative Fund Categories Retirees Sometimes Explore

(Educational examples only – individual suitability varies enormously)

Liquid Funds / Ultra-Short Duration Funds:

- For immediate emergency needs and 6-12 month cash reserves

- Virtually no volatility, high liquidity

- Returns typically 1-2% above savings account

- Risk-o-meter: Low

- Purpose: Emergency medical expenses, immediate cash needs, next 6-12 months’ living expenses

Short-Duration or Low-Duration Debt Funds:

- For stability with modestly higher returns than liquid funds

- Suitable for 1-3 year timeframe corpus

- Minimal interest rate risk due to short duration

- Risk-o-meter: Low

- Purpose: Years 2-5 of living expenses, planned major expenses (home repairs, appliance replacement)

Conservative Hybrid Funds:

- Majority debt (70-80%) with small equity component (20-30%)

- Equity portion provides long-term inflation protection

- Debt portion provides stability and withdrawal source

- Risk-o-meter: Low to Moderate

- Purpose: 5-10+ year timeframe corpus, balance between stability and inflation combat

Equity Savings Funds:

- Very low equity exposure (typically 20-30%) with built-in hedging mechanisms

- Designed specifically for conservative investors needing slight equity exposure

- Lower volatility than pure equity or even aggressive hybrid funds

- Risk-o-meter: Low to Moderate

- Purpose: Extremely conservative inflation protection for very long-term (10-20 year) corpus

Monthly Income Plans (Debt-Oriented):

- Primarily debt (85-95%) with tiny equity component

- Focus on regular income generation through dividend/SWP

- Very conservative

- Risk-o-meter: Low to Low-Moderate

- Purpose: Regular income generation with capital stability

The Withdrawal Challenge: Earning Returns While Taking Money Out

Here’s what many retirees don’t fully grasp until experiencing it: earning returns while systematically withdrawing funds is fundamentally different from accumulation.

During accumulation (working years):

- Market crashes are buying opportunities (buy low through SIPs)

- Time heals volatility wounds

- Can pause investments during emergencies

- Salary continues regardless of portfolio value

During withdrawal (retirement years):

- Market crashes accelerate portfolio depletion

- Time might not heal wounds before funds run out

- Cannot pause withdrawals (you need the money for living expenses)

- No salary safety net

Example of the withdrawal problem:

Year 1: ₹1 crore portfolio, withdraw ₹50,000 monthly (₹6 lakh annually = 6% withdrawal)

- Portfolio grows 8%, ending at ₹1.02 crore despite withdrawals

- Everything seems fine

Year 2: Markets crash -30%, portfolio drops to ₹71.4 lakh

- Still withdrawing ₹50,000 monthly (now 8.4% of smaller portfolio!)

- Selling more units at depressed prices to maintain same rupee withdrawal

- Portfolio ends year at ₹65.4 lakh

Year 3: Markets recover +20%, portfolio grows to ₹78.5 lakh

- But you’ve permanently sold units at low prices in Year 2

- Never fully recovered the 30% loss because of continued withdrawals

- Portfolio permanently impaired

This is why conservative allocation and reserves strategy are non-negotiable in retirement.

The Bucket Strategy: Managing Retirement Withdrawals Intelligently

Many financial planners recommend a “bucket” or “time-segmentation” approach for retirement portfolios:

Bucket 1: Immediate Needs (0-2 years)

- Allocation: Liquid funds, ultra-short duration funds, savings account

- Amount: 2-3 years of expected living expenses

- Purpose: All withdrawals come from here; zero market risk

- Rebalancing: Refill annually from Bucket 2

Bucket 2: Near-Term Needs (2-7 years)

- Allocation: Short-duration debt funds, low-duration debt funds, conservative debt funds

- Amount: 3-5 years of living expenses

- Purpose: Stable reserve to refill Bucket 1 annually; minimal market risk

- Rebalancing: Refill periodically from Bucket 3 during good market years

Bucket 3: Long-Term Growth (7+ years)

- Allocation: Conservative hybrid funds, balanced advantage funds, small large-cap equity allocation

- Amount: Remaining retirement corpus

- Purpose: Long-term inflation protection; never touched except to refill Bucket 2 during market upswings

- Rebalancing: Left untouched during market downturns; harvested during market peaks

How this protects you:

When markets crash 35%, you don’t care – you’re living off Bucket 1 (stable liquid funds). Bucket 3 (equity/hybrid) crashes, but you never need to sell those units at depressed prices. You wait 2-3 years for recovery while living off Buckets 1 and 2.

When markets recover strongly, you harvest some gains from Bucket 3 to refill Bucket 2, taking profits from appreciated assets.

This approach systematically implements “sell high, never sell low” – the opposite of what panicked retirees typically do.

Understanding Withdrawal Rate: The 4% Rule and Indian Context

A famous retirement planning guideline in the US is the “4% rule”: withdraw 4% of your initial retirement corpus annually, adjusted for inflation, and your money should last 30 years.

Example: ₹1 crore corpus → withdraw ₹4 lakh in Year 1 → ₹4.24 lakh in Year 2 (assuming 6% inflation) → etc.

Important caveats for Indian context:

- 4% assumes Western market returns and inflation: May or may not apply to Indian markets

- Doesn’t account for healthcare cost inflation: Medical expenses often rise faster than general inflation

- Assumes no other income: If you have pension/rental income, you can withdraw higher percentage

- Conservative for early retirees: If retiring at 55, 3-3.5% might be safer for 35-year retirement

- Aggressive for late retirees: If retiring at 65-70 with modest life expectancy, 5-6% might work

Critical point: Withdrawal rate is not “how much can I take” – it’s “how much can I safely take without running out during my lifetime.”

For personalized withdrawal rate analysis based on your specific corpus, expenses, other income, and life expectancy assumptions, consult a SEBI-registered investment advisor.

Common Retirement Portfolio Mistakes to Avoid

Mistake 1: Going 100% Conservative Too Early

- Missing 15-20 years of inflation protection

- Purchasing power erosion over long retirement

- Solution: Maintain 15-25% equity in large-cap/conservative hybrid for long-term portion

Mistake 2: Maintaining Too Much Equity Too Long

- Catastrophic losses right at retirement

- Forced selling during market crashes

- Solution: Start de-risking glide path in early 50s, not late 50s

Mistake 3: No Liquidity Reserves

- Forced to sell long-term investments for emergencies

- Selling equity during downturns

- Solution: Maintain 2-3 years expenses in liquid/short-duration funds always

Mistake 4: Withdrawing Same Rupee Amount Regardless of Portfolio Performance

- Accelerates depletion during poor market years

- Solution: Consider flexible withdrawal (reduce slightly during market downturns, increase during strong years)

Mistake 5: Not Accounting for Longevity

- Planning for 15-year retirement when you might live 25-30 years

- Solution: Stress test for age 90-95, not 75-80

Mistake 6: Ignoring Healthcare Cost Inflation

- General expenses rise 6%, healthcare might rise 10-12%

- Insurance premiums skyrocket after 60-65

- Solution: Maintain separate healthcare reserve, factor higher inflation for medical component

Assessing Your Own Situation: Honest Questions Every Investor Must Answer

Before investing in any mutual fund at any life stage, work through these questions with brutal honesty – not optimism, not what you wish were true, but what IS true:

1. Time Horizon Reality Check

Question: How many years until you actually need this specific money for the intended goal?

- Don’t answer “retirement is 25 years away” if you might need this corpus for child’s education in 7 years

- Don’t confuse multiple goals – each goal has its own timeline

- Don’t be optimistically vague – write specific dates

Example of honest assessment:

- Emergency fund: 0 years (needed immediately if emergency strikes)

- Daughter’s engineering admission: 6 years (she’s in Class 11)

- Son’s MBA: 12 years (he’s in Class 7)

- Retirement: 18 years (I’m 47, planning retirement at 65)

Each goal gets separate treatment with appropriate risk level.

2. Volatility Tolerance: Psychological Reality

Question: If your ₹10 lakh investment dropped to ₹7 lakh in three months, what would you actually do?

Be honest:

- “I’d panic and sell immediately” → Very low risk tolerance; “Low” Risk-o-meter funds only

- “I’d worry constantly, check portfolio daily, lose sleep” → Low-moderate tolerance; “Low to Moderate” funds

- “I’d feel uncomfortable but hold” → Moderate tolerance; “Moderate” funds

- “I’d feel fine, maybe invest more” → High tolerance; “Moderately High to High” funds

Reality check: Most people overestimate until experiencing real losses. If you’ve never lost 30% of your portfolio, you don’t know your true tolerance yet.

Follow-up question: Would that answer change if it was ₹1 crore dropping to ₹70 lakh? Absolute rupee losses hurt differently than percentage losses.

3. Emergency Reserve Assessment

Question: Do you have 6-12 months of living expenses in completely safe, immediately accessible accounts that are entirely separate from your investment portfolio?

- If NO: Stop here. Build emergency fund before investing anything in equity-oriented funds.

- If YES: Verify it’s truly liquid (savings account, liquid funds, short FDs – not locked insurance products or illiquid real estate)

Emergency fund is non-negotiable. Without it, you’ll destroy long-term investment strategy during first emergency.

4. Income Stability and Stress Testing

Question 1: If you lost your job tomorrow, could you cover all expenses for 6 months without touching investment portfolio?

Question 2: If your investment portfolio declined 30% over 6 months, could you maintain your regular SIP contributions without financial stress?

- If NO to either: Your actual risk capacity is lower than you think, regardless of your time horizon

- You might need more conservative allocation or larger emergency fund

Question 3: How secure is your income source?

- Government/PSU job: High security

- Established corporate role: Moderate-high security

- Startup/volatile industry: Moderate security

- Commission-based/freelance: Low security

Lower income security = lower practical risk capacity even with long time horizons.

5. Existing Corpus vs. Goal Requirements

Question: How much have you already accumulated versus how much more you need for each goal?

Example:

Goal: ₹1 crore retirement corpus needed

- Situation A: Currently ₹80 lakh accumulated (80% complete)

- Can afford lower risk (you’re close)

- Focus on preservation with modest growth

- Situation B: Currently ₹20 lakh accumulated (20% complete)

- Need higher returns to reach goal

- Can afford higher risk if time horizon permits

The closer you are to goal completion, the more you shift toward preservation over growth.

6. Financial Obligations Inventory

Question: What are your monthly fixed financial obligations?

Make an actual list:

- Home loan EMI: ₹_______

- Car loan EMI: ₹_______

- Children’s school fees: ₹_______

- Insurance premiums (monthly equivalent): ₹_______

- Parents’ support: ₹_______

- Other dependents: ₹_______

- Total fixed obligations: ₹_______

Compare to monthly income. Higher obligations relative to income = lower effective risk capacity.

Follow-up: What major expenses are coming in 3-5 years?

- College admissions

- Weddings

- Home down payment

- Major home repairs

These reduce your flexibility and effective risk capacity.

7. Current Portfolio Composition

Question: What’s your total current investment allocation across all accounts?

Many investors don’t realize they’re already overexposed:

Example:

- EPF/PPF: ₹15 lakh (debt/guaranteed)

- Real estate: ₹40 lakh (illiquid, location-specific)

- Gold: ₹5 lakh (alternative asset)

- Existing equity mutual funds: ₹12 lakh (equity)

- Insurance ULIPs: ₹8 lakh (mixed equity-debt)

- Total: ₹80 lakh

- Current equity exposure: About 25% (₹12L + portion of ULIPs)

Before adding “aggressive equity fund,” consider you might already be appropriately allocated when viewing complete picture.

The SEBI Risk-o-meter: A Tool, Not a Decision

Use SEBI’s Risk-o-meter on every scheme document – but remember:

✅ It tells you: This fund’s inherent volatility level

❌ It doesn’t tell you: Whether that volatility is appropriate for you

“Very High” risk fund might be perfect for some investors, terrible for others, even at same age.

The Gradual Risk Evolution Principle: Why Glide Paths Work

One of the most important principles in long-term investing – yet often ignored – is this:

Your risk level should evolve gradually and continuously over decades, not shift suddenly at arbitrary points.

The Wrong Approach (Too Common)

- Ages 25-55: Maintain 90% equity, ignore risk entirely

- Age 58: Suddenly panic about retirement proximity

- Age 59: Try to shift everything from 90% equity to 30% overnight

- Problem: Might be selling equity at terrible prices in crashed market precisely because you waited too long to start transition

The Right Approach: Glide Path Investing

Smooth, gradual, systematic reduction in risk over decades:

- Age 25: 85-90% equity (appropriate for 35-year horizon)

- Age 35: 75-80% equity (starting gradual reduction)

- Age 45: 60-65% equity (balanced growth and protection)

- Age 55: 40-45% equity (preservation with growth)

- Age 65: 20-25% equity (conservative with inflation protection)

Notice: The shift happens slowly, steadily, systematically over 40 years. No drama, no crisis, no sudden moves, no forced selling during bad markets.

Why Glide Paths Work

1. Removes Emotion: You’re not making panic decisions during market crashes – you’re following a pre-set plan

2. Captures Growth When You Can: Maintains higher equity when you have time to recover from volatility

3. Protects When You Can’t: Reduces equity as recovery time shrinks

4. Prevents Forced Selling: You’re not caught in a situation where you must sell equity during crashes because you waited too long to de-risk

5. Provides Peace of Mind: Your risk level always matches your changing capacity and life stage

Implementing Your Personal Glide Path

Step 1: Determine your current appropriate equity allocation based on age, goals, risk capacity

Step 2: Determine your target allocation at retirement

Step 3: Calculate annual reduction needed

Example:

- Current age 40, equity allocation 70%

- Retirement age 60, target allocation 25%

- Years until retirement: 20

- Required annual reduction: (70% – 25%) / 20 = 2.25% per year

- Implementation: Reduce equity by approximately 2% annually through rebalancing

Step 4: Set annual calendar reminder to rebalance according to glide path

Step 5: Stick to the plan regardless of market conditions

Important Caveat: One Size Does NOT Fit All

The percentages above are illustrative only. Your actual appropriate allocation depends on:

- Your complete financial situation

- Total corpus size

- Other income sources (pension, rental income)

- Life expectancy assumptions

- Risk capacity and risk tolerance

- Specific goal timelines

- Healthcare considerations

- Family obligations

For personalized glide path design specific to your circumstances, consult a SEBI-registered investment advisor.

When to Seek Professional Guidance

Everything in this article provides educational background – general principles about how risk levels typically relate to life stages.

But this is absolutely critical to understand: Your situation is unique. This article cannot – and should not – replace personalized professional guidance.

What This Article Cannot Do

❌ Assess your complete financial picture across all assets and liabilities

❌ Understand your family dynamics, health considerations, and personal circumstances

❌ Account for your specific goals with their exact timelines and rupee requirements

❌ Evaluate your genuine psychological risk tolerance based on your personality and experience

❌ Consider tax implications specific to your income level and tax bracket

❌ Recommend specific fund schemes appropriate for your exact situation

❌ Design a comprehensive financial plan integrating investments, insurance, estate planning, and retirement strategy

What Professional Advisors CAN Do

AMFI-Registered Mutual Fund Distributors Can:

✅ Assess your risk profile through detailed questionnaires and discussions

✅ Recommend specific mutual fund schemes matching your risk capacity and goals

✅ Explain fund characteristics, costs, and suitability

✅ Help with scheme selection across equity, debt, and hybrid categories

✅ Assist with account opening, KYC, transactions

✅ Provide ongoing service for portfolio reviews and rebalancing

Limitations: AMFI distributors are not registered as investment advisors. Their guidance is limited to mutual fund product selection, not comprehensive financial planning.

How to Choose Professional Guidance

For Mutual Fund Selection Only:

- AMFI-registered distributor is appropriate

- Check ARN registration at amfiindia.com

- Understand their commission structure (Regular vs Direct plans)

- Ask about commission disclosure for competing products

For Comprehensive Financial Planning:

- SEBI-registered investment advisor is appropriate

- Verify registration at sebi.gov.in (List of Registered Investment Advisors)

- Understand fee structure upfront

- Ensure advisor has fiduciary duty

For Tax Optimization:

- Consult Chartered Accountant in addition to investment advisor

- Tax laws change; professional guidance ensures compliance and optimization

Questions to Ask Any Financial Professional

Before engaging any advisor or distributor:

- Credentials: What are your qualifications, certifications, and registrations? (Ask for registration numbers and verify independently)

- Experience: How long have you been advising clients? What’s your area of expertise?

- Compensation: How are you compensated? Commissions, fees, or both? From which sources?

- Conflicts: What potential conflicts of interest exist? (Commission-based distributors have inherent conflicts)

- Services: What exactly is included in your service? Ongoing reviews? Rebalancing? Tax planning?

- Process: What’s your investment philosophy and client service process?

- References: Can you provide references from long-term clients with similar situations?

Red flags:

- Guarantees of returns

- Pressure to invest immediately

- Reluctance to disclose compensation

- Cannot verify registrations

- Promises that sound too good to be true

The Bottom Line

Your financial future deserves professional input. The cost of professional guidance – whether distributor commissions or advisor fees – is typically far less than the cost of major mistakes made from going it alone.

This article equips you with knowledge to have informed conversations with professionals, not to replace those professionals entirely.

Important Disclaimer and Regulatory Disclosures

Regulatory Notice

Mutual fund investments are subject to market risks. Please read all scheme-related documents (Scheme Information Document, Statement of Additional Information, Key Information Memorandum, Annual Report) carefully before investing.

Educational Content Only – Not Investment Advice

This article provides educational information about how mutual fund risk levels generally relate to different life stages based on common financial planning principles. It does not constitute:

- Investment advice, recommendation, or personalized guidance

- A recommendation to buy, sell, or hold any specific mutual fund scheme

- A solicitation to invest in any particular product or fund house

- Personalized financial planning tailored to your circumstances

The life-stage framework presented here is illustrative and educational only. It does not guarantee suitability for your personal circumstances, which may differ dramatically from general patterns.

Past Performance Disclaimer

Past performance of any mutual fund, fund category, or investment approach is not indicative of future results. Market conditions, economic factors, fund management quality, and individual fund performance vary significantly, unpredictably, and continuously.

Historical return ranges mentioned (such as equity SIP returns over long periods) represent past outcomes during specific historical market conditions. These past outcomes:

- Do not predict or guarantee future performance

- May not repeat in different market environments

- Can vary dramatically based on specific time periods selected

- Represent averages that mask significant year-to-year volatility

Actual future returns may be substantially higher or lower than any historical patterns, including negative returns over extended periods.

No Guarantees or Assurances

No investment strategy, allocation approach, or mutual fund category guarantees returns or protects against losses.

- Equity funds can experience losses of 30-60% during severe market downturns

- Debt funds can experience losses due to interest rate changes or credit events

- Hybrid funds can experience losses during adverse market conditions

- Even “Low” risk funds carry some market risk

Actual investment outcomes can differ dramatically from:

- Historical patterns

- Theoretical expectations

- Illustrative examples in this article

- Average or expected returns

All mutual fund investments carry risk of capital loss. Returns are not assured, guaranteed, or predictable.

Tax Considerations

Tax treatment of mutual fund investments varies significantly by:

- Individual circumstances

- Total income level

- Applicable tax brackets

- Other income sources

- Applicable tax laws, which change periodically through legislative action

Tax rates, exemption limits, deduction availability, and holding period requirements mentioned in this article are based on laws applicable for FY 2025-26 and are subject to change.

For tax guidance specific to your situation, consult a qualified Chartered Accountant or tax professional. Do not make tax-related decisions based solely on this article.

Individual Circumstances Critical

The appropriateness of any investment depends entirely on your complete personal financial situation, including:

- Risk capacity (ability to bear losses without financial hardship)

- Risk tolerance (psychological comfort with volatility)

- Time horizon to specific goals

- Financial goals and their priorities

- Existing portfolio and asset allocation

- Financial obligations and dependents

- Income stability and growth trajectory

- Emergency reserves and liquidity needs

- Health circumstances and insurance coverage

- Age, life stage, and family situation

- Tax bracket and tax planning strategies

Do not make investment decisions based solely on this article, your age, or generalized life-stage frameworks. Seek personalized professional guidance.

Regulatory Information and Investor Protection

For current information on SEBI regulations, investor protection, and grievance redressal:

- Securities and Exchange Board of India (SEBI): https://www.sebi.gov.in

- SEBI SCORES platform for investor complaints

- List of registered Investment Advisors

- Investor education resources

- Association of Mutual Funds in India (AMFI): https://www.amfiindia.com

- Verify distributor ARN registrations

- Investor awareness resources

- Industry standards and best practices

Limitation of Liability

The author provides this educational content without any warranties, express or implied, regarding accuracy, completeness, or suitability for any particular purpose. The author shall not be liable for any losses, damages, or adverse outcomes arising from reliance on this article or decisions made based on its content.

Investment decisions are solely your responsibility and should be made only after:

- Thorough personal assessment

- Professional consultation

- Careful review of all fund documents

- Understanding of all risks involved

About the Author

Author Credentials

Amit Verma – AMFI-Registered Mutual Fund Distributor

AMFI ARN: 349400 (Distributor Registration Number)

Verification: You can independently verify this registration at amfiindia.com:

Your Choices:

- You are completely free to invest through me, another distributor, or directly with fund houses

- Compare my services and commission structure with other distributors if desired

- Choose Direct Plans to completely eliminate distributor commissions (requires you to select schemes independently)

- No obligation to use my services simply because you read this article

Transparency Commitment:

- I will disclose my approximate commission percentage on any recommended scheme upon request

- I will explain differences between Regular and Direct Plans before you invest

- I will not discourage you from choosing Direct Plans if you prefer to invest independently

My Regulatory Limitations

What I Am NOT:

- I am NOT registered with SEBI as an Investment Advisor

- I cannot provide comprehensive, holistic financial planning across all asset classes

- I cannot provide personalized investment advice that constitutes formal advisory services

What I Can Provide:

- Mutual fund product selection assistance based on your stated risk profile and goals

- Scheme recommendations within mutual fund category

- Transaction assistance, account opening, KYC support

- Ongoing service for portfolio reviews and rebalancing within mutual fund products

- Educational content like this article

Limitations on Advice:

- My recommendations are limited to “incidental advice” to aid your scheme selection

- I operate under AMFI guidelines for distributors, not SEBI’s stricter advisor fiduciary standards

- For comprehensive financial planning, you should consult a SEBI-registered investment advisor

Regulatory Compliance

As an AMFI-registered distributor, I am required to:

- Disclose my ARN on all communications (ARN-349400)

- Provide scheme-related documents before you invest

- Conduct basic risk profiling before recommendations

- Not guarantee returns or make misleading statements

- Follow AMFI’s Code of Ethics for distributors

Contact Information and Resources

For Questions About This Article

If you have questions about mutual fund concepts, life-stage investing principles, or general educational clarifications:

- Website: mfd.co.in

- Phone: +91-76510-32666

- Email: planwithmfd@gmail.com

")

Forget It” Retirement Plan")

{kind=link}